THE ULTIMATE BEGINNER’S GUIDE

Let’s face it… investing in residential real estate is fast becoming a favourite pastime here in Australia, as the traditional Great Australian Dream starts to revolve as much around housing as a commodity, as it is a home to live in.Given that investment grade property is capable of consistently delivering combined annual returns in the region of 13 per cent plus (average 8% capital growth plus 5% rental yield), it’s hardly surprising that more of us are turning to bricks and mortar in a bid to secure our financial future.

PROPERTY INVESTMENT IN AUSTRALIA

A BRIEF HISTORY OF AUSTRALIAN PROPERTY INVESTMENT

Australia’s property markets have always been somewhat unique, compared to other developed economies.

For one we’ve demonstrated a historical preference for sprawling outwards across vast suburban housing estates, instead of building towering residential high-rise accommodation centered entirely in and around our major city centres. At least up until recently that is.

Baby boomers have arguably been the most influential generation on the evolution of Australian real estate.

After watching their parents struggle through two World Wars and a Great Depression, older boomers longed for a sense of stability and found it in the ideal of home ownership, which took hold in the collective cultural psyche of our nation.

Buying one’s own home became an aspirational symbol of personal success, as we started to lead the world in a trend of strong home ownership rates that have long hovered around 70 per cent.

The concept of real estate as a tradable commodity really took off late last century, and since the 1980s our interest in property investment has continued to snowball, helped along by various factors that have stimulated strong market growth and investment activity.

THE POLITICS OF PROPERTY INVESTMENT

Politically speaking, housing has become an essential aspect of our national prosperity.

Each successive government has become increasingly reliant on revenue generated by this sector in the form of stamp duties, land taxes and the like, as well as the flow on positive impact it can produce across the broader economy, to sustain us through the ups and downs that ensue across a global financial market.

This was glaringly apparent when, during the 2008 Global Financial Crisis that knocked many super-sized world economies off their feet and saw major property markets crumble, Australia’s federal government started throwing money at first homebuyers to jump into real estate and keep the sector stimulated.

The ploy worked, and as share markets took a hammering, most pockets of our property markets kept ticking along quite nicely, with only a leveling out or very slight correction throughout most of our cities and suburbs.

PROPERTY INVESTMENT’S NEW BLOOD

If there was any doubt that property was the most reliable and ‘risk friendly’ investment vehicle for Aussie mums and dads to secure their financial future, it was quickly eliminated by the GFC and the devastating losses many households experienced across the sharemarket at the time.

Property investment understandably grew in popularity, and a whole new generation watched as their parents attempted to claw back life savings lost in stocks, through a much more steadfast real estate market.

Children of the younger baby boomers and older Gen Xers have witnessed real estate do nothing but rise throughout their young lives.

They have never been privy to any devastating, firsthand price corrections and in some instances; the homes their grandparents purchased back in the day for $30,000 are now worth 50 times that much.

Hence we’re seeing a rising trend among young, would-be homeowners, who are choosing to forego their own ‘Great Australian Dream’ in order to become professional property investors and landlords.

Anecdotal industry reports from the past two to three years suggest that more Gen Y’s and so-called Millennials are opting to rent in their most desired inner city locations, close to the action but where price entry points are too prohibitive for first time buyers.

Cleverly, these ‘youngblood’ investors are securing more affordable investment property slightly further out from the CBD, with plans to leverage into more property assets over time and eventually acquire their own dream, inner city pad.

PROPERTY INVESTMENT BECOMES A SUPER IDEA

Further bolstering the rate of bricks and mortar investment dealings over the past ten or so years has been a push for more working Australians to assume control of their retirement savings, in the form of Self Managed Super Funds (SMSFs).

mAustralia faces numerous challenges as a rapidly ageing and expanding population, with predictions that we’ll soon see a scenario whereby for every three tax paying residents (aged between 15 and 64 years), there’ll be one 65 plus year old exerting pressure on publicly funded services.

The government recognises that property investment could be one good solution to a number of these issues.

According to its latest Intergenerational Report, Australia’s population is expected to reach almost 40 million by 2055, with nearly a quarter of that number over the age of 65.

This means we’ll need a lot more accommodation to house our growing numbers and we need to be smarter about how and where we build it, as new infrastructure spending must be minimised wherever possible in order for funds to be directed according to population needs – presumably healthcare and education.

It’s also anticipated that a lot of the social welfare benefits many middle-income households currently rely on could be clawed back. Alarmingly, this includes concerns around the sustainability of the government paid aged pension as it exists today.

The key message is you need to be in charge of your own financial destiny. If you want a retirement worth working for, then jump in the driver’s seat, define your goals and work out how you plan to get from A to B.

Oh…and don’t think you can necessarily rely on that traditional, managed super fund…as many Australians who were fast approaching retirement found out when they lost their nest eggs to the GFC juggernaut.

Just before that fateful world economic correction in 2008, the government legislated that SMSF structures could obtain credit to acquire real estate in the form of limited recourse borrowing, which had not previously been possible.

Both these revisions and a few new niggling doubts about who to trust with the management of your finances, were enough to catapult the concept of SMSFs from the realm of a privileged, cashed up few to a widely accessible ‘mum and dad’ option for self funding retirement.

According to latest figures from the Australian Taxation Office, residential property holdings within SMSFs increased by 17 per cent in the year to March 2014, from $17.5 to $20.5 billion, and are currently estimated to be worth around $21.6 billion.

Although housing accounts for a disproportionately small number of overall assets, at just 2.5 per cent of the total $590 billion invested in SMSFs, it’s clear from the growing tide of SMSF property advisory businesses and products flooding the market that this is a steadily growing sector.

THE IMPACT OF A LOW INTEREST RATE ENVIRONMENT ON PROPERTY INVESTMENT

As our economic outlook started weakening off the back of a steadily slowing resources sector back in 2012/13, the Reserve Bank began cutting interest rates. At time of writing, the official cash rate sits at a low 2.0 per cent and has been hovering around this figure for months now.

This low interest rate environment, along with all the above-mentioned variables, has brought about a tidal wave of activity that’s arguably eclipsed the property investor groundswell of 2002-03.

HOW MANY AUSTRALIANS INVEST IN PROPERTY?

According to data from the Reserve Bank, the number of property purchases attributable to investors has been steadily climbing over the last two decades.

But industry analysts say nothing compares to what we’ve recently witnessed, with investors accounting for an estimated 50 per cent of all mortgages taken up across the inner city Sydney and Melbourne markets particularly.

According to ATO data, the share of population aged 15 years and over with an investment property grew steadily throughout the 1990s and early 2000s, stabilising at around 10 per cent late last decade.

But experts predict this figure will increase when next revised, due to the latest boom phase.

Importantly, not everyone who’s actively investing right now will realise the lofty heights at the top of the property ladder…and ultimate financial freedom.

In fact statistics suggest that less than one per cent of people who try their hand at real estate investment will own six or more properties – enough to comfortably fund their desired retirement lifestyle.

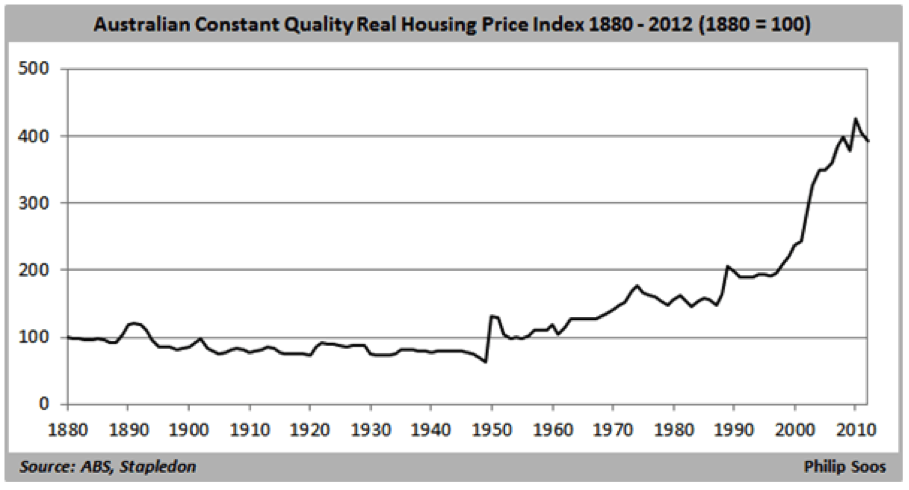

HISTORICAL PRICE GROWTH OF PROPERTY

It’s little surprise that Australians have evolved into a nation of real estate enthusiasts when you look at the sector’s historical rate of price growth across our major cities.

As we have become increasingly enamoured with the idea of bricks and mortar to secure our financial future, we’ve added to the buoyancy of this asset class.

It’s virtually impossible to deny the logic of property as a reliable commodity when you consider the long-term capital growth averages…

Very few markets have enjoyed such a relatively steady upward trajectory for sixty plus years. Yes, there have quite clearly been some ups and downs, as well as peaks and plateaus, but real estate has invariably managed to pick itself up and dust itself off after every one.

And more to the point…when you buy quality, investment grade housing assets, these fluctuations are diminished even further.

It’s all fairly relative in real estate. The more desirable and in demand your piece of dirt is and the less of it there happens to be…the stronger the long-term value gains you can anticipate.

In fact experts will tell you that investment grade assets can deliver above average returns, generally doubling in value every seven to ten years; or the time it takes for one full market cycle to play out.

The value of real estate essentially comes down to a number of enduring fundamentals, with location being right at the top of the list.

This is very apparent when you consider that some parts of our inner cities will double in value quicker than neighbourhoods ‘on the other side of the tracks’, for instance.

One example is Sydney’s iconic beachside suburb of Tamarama, where buyers are drawn to the area’s exceptional livability due to proximity to both the CBD (just 10 kms) and popular city beaches, as well as an underlying air of affluence among the locals.

According to figures from RP Data, the median house price in Tamarama increased from $455,734 in November 1998 to $4.4 million in November 2008. Over one decade, the suburb averaged a massive growth rate of 25.45% per annum!

Or 865% across ten years.

On the other hand, Liberty Grove – another Sydney suburb just 17 kilometres from the CBD, but minus the direct rail access and waterfront location, enjoyed average annual house price growth of just 4.2 per cent for the same ten-year timeframe.

Its median property values rose from $362,663 in November 1998 to $547,500 in November 2008.

One thing these vast differences in numbers demonstrate is that you have to be incredibly careful about asset evaluation and selection.

Past performance is a good indicator of future potential in premium property markets. Likewise if you try to buy a bargain, you might found out the hard way that it’s cheap for good reason.

TAX IMPLICATIONS OF PROPERTY INVESTMENT

One of the primary reasons many people toy with the idea of property investment to secure their financial future is the unique associated tax savings, which can assist in covering holding costs and sustaining your portfolio over the long term.

But it’s not all about the government giving money back to you as a property investor. There are also taxes you’ll be required to contribute when transacting real estate.

The good news is, although your rental income will attract the same nominal rate of tax applied to your personal income (depending on ownership structure), any capital raised over time isn’t subject to tax unless it’s liquefied (or sold).

Now let’s take a closer look at the various tax allowances and liabilities you’ll encounter on your property investment journey…

NEGATIVE GEARING AND OTHER DEDUCTIBLE COSTS

We mentioned previously that negative gearing is where the interest payable on an investment loan for income producing property can be claimed in full as a legitimate tax deduction. The shortfall is offset in the property investor’s taxable income, including your salary and any rent received from your asset.

Negative gearing is one method smart property investors use to help manage cashflow, often using the return they receive at tax time to help pay down debt and sustain their portfolio.

You can also claim a number of expenses associated with maintaining and managing your property investment(s), such as repair and improvement costs and property management fees. These are known as deductible items.

DEPRECIATION ALLOWANCES

Another good way to shore up income and claw back your debt to the government each financial year is through depreciation benefits. In real estate it’s widely held that land appreciates in value over time, while the house on it loses value as it physically deteriorates. This means you can claim depreciation.

You’ll require the services of a Quantity Surveyor, who’ll inspect the premises, list all depreciable items and their anticipated losses over a designated period and provide a full report for your accountant to claim as many deductions on your behalf as possible

SEEK ADVICE AND GET IT RIGHT

The take home message for beginning property investors is to seek professional counsel and with the appropriate advice aligned with your needs, determine the best investment strategy(s) and structure(s) to safely and successfully reach your wealth creation goals.

Before you’re ready to actually buy an investment property, you need to think long and hard about who will own it and why. Remember, it should never be entirely about the tax savings. Your focus must be on the potential for profit and return at all times, not on how much you might lose.

Importantly, these decisions need to complement your own needs and objectives, in accordance with your long-term financial plans.

If an ‘advisor’ starts telling you about the ‘prefect’ structure, strategy or product, without first taking an extensive account of your financial situation and wealth creation goals, ask yourself who will really be deriving benefit from the ‘advice’ you’re receiving.

PROPERTY FINANCE

Australia’s lending landscape is undergoing a significant transformation at time of writing, with property investors front and centre of a financial services sector in the midst of a regulatory overhaul. It started a couple of years ago when…

Australia’s lending landscape is undergoing a significant transformation at time of writing, with property investors front and centre of a financial services sector in the midst of a regulatory overhaul. It started a couple of years ago when…

- In August 2013, the RBA cut the official cash rate to 2.5% from 2.75%, where it had been sitting since an unprecedented drop from 3% in May 2013.

- Property investment was already proving popular at the time, but interest rates below 3% and the ensuing ‘cheap credit’ to be had were just too much of an enticement, as more and more equity laden baby boomers and Gen X-ers entered the property markets.

- Many focused their attention around inner city Melbourne and Sydney in particular. With the latter city having done very little in terms of house price growth for some ten years, after the early 2000s property boom.

Prices in both markets started to rise…but for Sydney, where activity levels had been fairly moderate for quite a while, things took off in a big way as the existing accommodation undersupply experienced further pressure from renewed demand.

A slowing resources sector helped this process, as more employment opportunities opened up around the many service-based industries located in and around the Harbour City.

- Increasing talk of a housing bubble had many economists and policymakers worried, including the Reserve Bank of Australia and regulators like the Australian Prudential and Regulatory Authority (APRA).

Of course the RBA has been forced to reduce rates further over the last two years, with the official cash rate having been at 2% for 6 months (at time of writing). In effect, the central bank’s inability to increase rates has helped to stimulate the very activity it’s concerned about.

- At the end of 2014, APRA stepped in to caution lenders about the rapid growth of their investment borrowing activity, politely suggesting they cap growth at 10% of their overall mortgage books. This was an attempt to put the brakes on Sydney’s property market, where quarterly double-digit gains were becoming the norm.

- Since then, lenders have been accused of not taking APRA’s warnings around ‘macroprudential policy’ (where the regulator starts to impose restrictions on banking loan practices) seriously enough and more official changes have been made.

- In a bid to reduce the risk of exposure for Australia’s financial sector to any type of future international economic crisis, APRA is now insisting that investment lending remain below the 10% threshold and that credit institutions hold more capital against their mortgage books.

- In response, lenders have started to increase interest rates across the board on their variable home loan products, in what they claim is a move to raise additional funds to meet the new capital requirements.

Serviceability criteria are also changing, as questions have arisen with regard to how thoroughly lenders are qualifying property investment borrowers (considered ‘higher risk’) in particular.

This essentially means that, now more than ever, property investors must have a well thought-out financial strategy in place and a loan portfolio that allows you full control over your asset, with the flexibility to evolve your real estate retirement fund according to your own objectives and timeline…not your bank’s!

NAVIGATING THE FOUR ‘CS’ OF CREDIT

While you might feel a little worried about your prospects for obtaining property investment finance in this new look lending landscape, rest assured that understanding some basic principles of the loan process will drastically improve your chances of securing finance.

Once you’re aware of these fundamental rules you’ll be able to safely navigate any type of lending terrain, whether you aim to own one investment property or several. So here are the four Cs of credit that every lender refers to when assessing mortgage applications…

-

CHARACTER

This is about you as a borrower and the potential risk you represent to the lender if they choose to give you finance. Under the spotlight will be things like:

- Your past borrowing and repayment history

- Professional and personal stability (how much you’ve changed employers and addresses)

- Your current Statement of Position (assets and liabilities)

- Your overall credit profile.

It’s important to maintain a clean track record when it comes to paying things like utility bills and loan instalments on time, as anything you overlook in this regard will show up on your credit file.

-

CAPACITY

Or whether you can service the loan, is the area that has recently been highlighted as cause for concern when it comes to assessing a borrower’s potential ‘risk weight’.

Obviously, the bank needs to know you can pay them back. So what do lenders look for when assessing serviceability?

- Once more employment history and stability come into play, as well as how much you earn.

- Future earning potential will also be considered, particularly if the property you’re financing is an investment and will therefore generate its own portion of income by way of rent.

- Rental income (current and projected) is accounted for, but only a portion of anywhere between about 60 to 80%, depending on the lender’s own internal rules.

- Your living expenses and any other loans you have to repay.

It’s important to note that things like credit card LIMITS, not just the debt you might owe, can significantly reduce your serviceability. As such, it’s advisable to keep personal, non-productive debt to a minimum and maintain a very low credit limit wherever possible.

-

CAPITAL

How much upfront cash do you plan on contributing to the deal? The deposit you provide is essentially the bank’s barometer that measures how committed you are to the acquisition and therefore, how much risk you’re prepared to assume alongside them.

It comes down to a simple equation – the lower the funding you request as a portion of the property’s purchase price (known as the Loan to Value Ration or LVR), the less inherent risk there is in the bank providing you with credit.

In other words, you’re more likely to receive approval for a property mortgage when requesting to borrow say, 60% of the purchase price as opposed to 100%. In fact, you’d be hard pressed to find a lender nowadays who’d approve a 100% LVR under any circumstances.

Further, if you propose to contribute less than 10% of the property’s value, the lender will make you take out Lender’s Mortgage Insurance or LMI, which covers them for any potential loss if forced to recover debt through the sale of your asset(s).

It’s long been held and still holds true today, that a decent deposit can get virtually any loan application over the line and often means more bargaining power.

-

COLLATERAL

This is the security you’re offering the banks in the form of the property itself, or in the case of cross-securitised loans – which you ideally want to avoid – multiple properties.

Depending on the type of asset and where it’s located, the bank will determine an appropriate maximum LVR they’re prepared to agree on, with and without the need for LMI.

This calculation is based on how easy it would be to liquefy the asset in any type of market conditions, should the need to recover on a mortgage default arise. In other words…how quickly can they offload the property and recover their capital?

The bank appoints a valuer to determine how much a property is worth before approving the loan. They will assess comparable sales in the area, as well as marketability potential for the property based on supply and demand fundamentals, before attributing a value to it.

That’s why the broader your property’s market appeal in terms of purpose, use and desirability, the better your chances at securing a higher bank valuation and therefore, more favourable LVR and other finance conditions.

On the flipside if you invest in ‘purpose built’ products, such as student accommodation, you limit your market and therefore, the ‘saleability’ and liquidity of the collateral on offer. You can see how this might make the banks think twice about providing finance.

DON’T GET A LOAN ALONE…

A number of professional mortgage brokers offer specialist property investment advice and assistance with identifying and applying for the best type of loan product these days.

Many have vast networks within the financial services sector and panels of preferred lenders, with well established industry affiliations and insights that can assist property investors in creating more accommodating finance portfolios.

Not to mention the insider knowledge that many borrowers walking in from ‘off the street’ would simply not be privy to, particularly when it comes to how each lender navigates the four C’s of serviceability.

WHERE TO START YOUR PROPERTY INVESTMENT JOURNEY

We trust that having reached the end of this definitive, beginner’s guide to property investment, you’re ready to take the proverbial bull by the horns and start climbing the property ladder all the way to the pinnacle of financial freedom.In property though, time is money.

We trust that having reached the end of this definitive, beginner’s guide to property investment, you’re ready to take the proverbial bull by the horns and start climbing the property ladder all the way to the pinnacle of financial freedom.In property though, time is money.

Property is unique in that its value can be leveraged without being liquefied, meaning you can keep borrowing against the growing value of your assets to purchase further high growth housing investments as time and money work their combined magic.

Therefore, in order to really reap the financial benefit you need to start as early as you possibly can and accumulate the best possible assets you can, which grow significantly in value whilst yielding sufficient cashflow to be sustainable.

You also need to be mindful of maintaining enough structural flexibility within your property and loan portfolios to enable optimal growth of your asset base, according to your identified needs.

This might all seem a bit daunting to anyone looking to just kick off their investment endeavours. But rest assured, in our digital day and age there’s an abundance of property investment resources to guide your journey, all the way from start to retirement…

PROPERTY INVESTMENT BOOKS

Online and hardcopy books covering all facets of property investment are readily available, with no shortage of so-called ‘experts’ ready to weigh in on the subject. Just be wary of self-proclaimed investment professionals who peddle property investment products or propaganda.

Good books are a good starting point to learn more about the strategies you can adopt as a property investor, with many works penned by people who have lived the experience and are now choosing to share their knowledge with others.

PROPERTY INVESTMENT ADVISORS

Nowadays it’s difficult not to find someone who thinks they know a thing or two about investing in property, particularly at family gatherings and backyard barbecues.

But if you plan on seeking investment advice from your Uncle John who hasn’t actually acquired his own fortune through real estate, you perhaps should reconsider whether this investment vehicle is right for you!

Paying for a professional opinion on property investment might be difficult to consider…particularly given that advisors fees can seem quite high…but the potential cost of getting your acquisition wrong can be financially devastating.

Just be careful to qualify anyone providing advice and make sure you separate the true investment expert from the thinly veiled salesperson looking to make a commission.

PROPERTY INVESTMENT SEMINARS & FORUMS

A similar disclaimer as above applies to any real estate forums or seminars you might attend. If you’re going to be pressured into signing up for an apartment or some other type of property related holding at the end, be very mindful of the advice being dished out and whether there’s an ‘angle’.

That being said, there are many credible property industry experts who do the ‘seminar circuits’ across our wide brown land, and many have a lot of interesting experience and insight to impart.

Plus, as with a lot of the resources used to further your property investment career; the cost to further your education within these forums is often tax deductible.

PROPERTY INVESTMENT RESEARCH

At the end of the day, people who choose to invest in property to secure their financial future have decided it’s time to take and keep control of their own destiny.

They want to be answerable to no one but themselves and their families when it comes to determining how hard and for how long they work, when they retire and what they do with their downtime…

It’s not surprising that many successful property investors end up becoming industry professionals in their own right. They’ve often done years of research whilst following their own investment trajectory and know what works and what doesn’t from years of personal experience.

With so much market information and data available at our fingertips, researching residential real estate for investment purposes has never been easier.

Remember though…the only way you’ll accumulate sufficient wealth with which to retire through property investment is by taking action.

Read the books, attend the seminars, seek advice and research the markets…but don’t become a professional ‘would-be’ investor who never makes a start. Why wait, when you can start now? It’s never been easier.