Positive Cash Flow Investment Property is property that pays you every week, just to own it.

That might sound great (and it certainly can be), but there is much more to cash flow positive property investment than meets the eye.

In this article, we’ll explore what cashflow positive is (and is not), as well as cover off some of the benefits and risks of when buying cash flow positive real estate.

So let’s get started.

Table Of Contents:

- What is Positive Cash Flow Property?

- Positive Cashflow Investment Property Example

- Positive Cash Flow vs Positive Gearing Explained

- Positive Cash Flow vs Negative Cashflow Explained

- Top 5 Benefits Of Cash Flow Positive Property

- Top 7 Risks and Pitfalls To Avoid

- Where To Find Positive Cashflow Properties?

- Positive Cash Flow Property Due Diligence Checklist

- How To Take The Next Steps

1. What is Positive Cash Flow Property?

Definition: Positive Cash Flow Property is an investment property where the annual rent exceeds the total annual expenses, after tax deductions and depreciation are taken into account.

In other words, this is a type of investment asset that “pays you” to own it.

The potential advantage of cash flow positive property is that it doesn’t drain your household income. In fact, quite the opposite.

Earning an annual income from your property is one advantage. The other is that you also have the potential to make a capital gain as the value of your investment property goes up over time.

Let’s make this more concrete with a specific example:

2. Positive Cashflow Investment Property Example

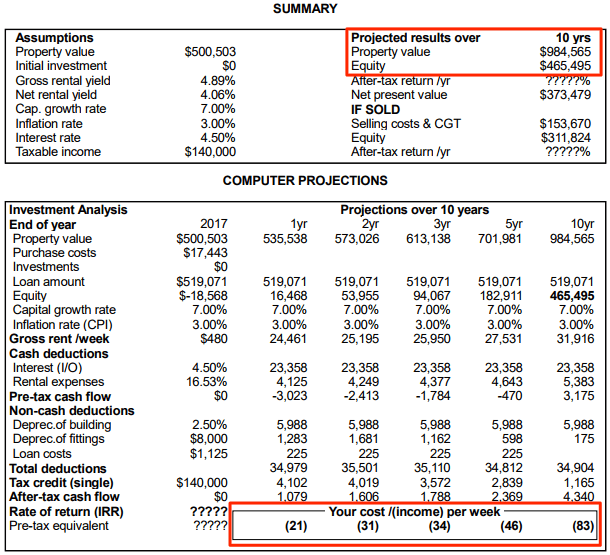

Here’s an actual screenshot of a property investment financial model presented to a client. In this case, the property is strongly cashflow positive.

(There are many factors that go into selecting the right property, and your situation may well be different from this investor. This example is just for illustration purposes.)

OK, let’s unpack this example:

- The purchase price is $500,503

- The gross rent per week is $480, or $24,461 per year after allowing for a 2% vacancy rate

- The loan interest is $23,358 in year 1, and other rental expenses amount to $4,125, giving a pre-tax cash flow of minus $3,023.

- However, there are additional non-cash deductions in the form of depreciation of the building and fittings, plus loan costs, which add up to a further $7,496 in year 1. Non-cash deductions mean tax deductions that you can legally claim, but don’t need to fund out of your own pocket in the form of cash.

- With $24,461 in total income and $34,979 in both cash and non-cash expenses, the on-paper “loss” in year 1 is $10,518.

- This on-paper loss enables the investor to claim a further $4,102 in tax back from the taxman.

- Overall, the after-tax cash flow of this property is therefore $1,079, or $21 per week in year 1.

Positive Cashflow That Increases Over Time

As you can see, the model predicts that the positive cash flow will actually increase over time, as rental increases and other factors are taken into account.

- In year 1, it’s $21 per week in positive cash flow.

- In year 2, it’s $31 per week in positive cash flow.

- In year 3, it’s $34 per week in positive cash flow.

- In year 5, it’s $46per week in positive cash flow.

- In year 10, it’s $83 per week in positive cash flow.

Now, $21 per week or even $83 per week may not sound like sums of money that will make you rich, but you have to remember that these cash flow figures are money-in-the-pocket, after ALL expenses have been paid.

Meanwhile, in the background, the property is appreciating in value.

According to this model, this property will accumulate $465,495 in equity in 10 years’ time.

(Not a bad return, considering the property is profitable to hold every year on the way through!)

Now that we’ve covered an example of what Positive Cash Flow Property IS, let’s look at how this strategy differs from two other often confused terms…

3. Positive Cash Flow vs Positive Gearing Explained

Positive Cash Flow describes a property that puts money in your pocket after all costs AND tax deductions, including depreciation, have been taken into account.

Positive Cash Flow describes a property that puts money in your pocket after all costs AND tax deductions, including depreciation, have been taken into account.

However, Positively Geared Property refers to property that delivers a cash surplus outright, BEFORE taking into account non-cash deductions such as depreciation.

Here’s a simple (hypothetical) example to illustrate:

- A property is purchased for $500,000

- All expenses are $30,000 per year

- The rental income is $650 per week over 50 weeks of the year, or $32,500 per year

- This property is said to be positively geared to the tune of $2,500 per year

- (Adding applicable non-cash deductions would make the numbers even more attractive, but this property is positively geared prior to doing this).

Positively geared property sounds great in principle, but it is usually difficult to buy property that is positively geared from day 1 and that ALSO has decent capital growth prospects.

That being said, many properties BECOME positively geared over time.

This is because as rents increase over time due to inflation and rises in rental demand, the income of a property investment typically increases until the property becomes positively geared.

(In the financial model above, you can see how in year 10, the property is producing $3,175 in pre-tax cash flow. At this point, the property is positively geared.

4. Positive Cash Flow vs Negative Cash Flow Explained

The flip side of positive cash flow is negative cash flow. Like the name implies, a negative cash flow property is one that costs you money to hold.

The flip side of positive cash flow is negative cash flow. Like the name implies, a negative cash flow property is one that costs you money to hold.

(In Australia, the total loss can be offset against the investor’s personal income tax liability, in what is known as negative gearing.)

One has to ask the question, “Why would an investor lose money every week on a property they own?”

The answer is, once the future capital growth is taken into account, they are predicting that they’ll be better off overall.

However, on the way, the investor has to wear the cash being sucked out of their wallet every week.

There’s also a risk that negative cash flow may hurt an investor’s ability to add more property assets to your portfolio, which is one reason why 7 out of 10 investors never get past property #1.

Property values have appreciated in Australia to the point where many properties in urban areas in particular are negative cash flow.

5. Top 5 Benefits Of Cash Flow Positive Property

Acquiring the right positive cash flow property can have many advantages for the investor:

Acquiring the right positive cash flow property can have many advantages for the investor:

- Self-Sustaining: Positive cash flow properties pay for themselves without requiring you to tip in money on a regular basis

- Scalable: the extra cashflow enables you to invest in more than one property at a time and/or buy your next property sooner

- Achieve your goals faster: Positive cash flow properties increase your income and therefore your ability to buy your next property sooner. It’s like a flywheel that’s spinning faster and faster.

- Reduced Cash Flow Risk: Positive cash flow properties are stand-alone. If something unforeseen were to happen to your income, you’re far less likely to have to sell your investment. Negatively geared properties cost you money to hold, and the moment your income drops, you can find yourself short of money and in a position where you have to sell quickly.

- Double Whammy Effect: cash flow positive properties enable you to lock in weekly cash flow, while ALSO gaining exposure to upside capital growth. For this reason, many investors prefer this strategy.

That’s the upside – but what about the potential downside and how to protect yourself?

6. Top 7 Risks and Pitfalls To Avoid

Positive Cash Flow Property can be a lucrative strategy for investors, but like all property investment strategies, how you execute is also critically important.

Positive Cash Flow Property can be a lucrative strategy for investors, but like all property investment strategies, how you execute is also critically important.

Buying the wrong type of positive cash flow property is worse than not investing at all. Here are a few of the risks and traps to watch out for:

- Beware of High Risk Property Types: certain property types such as serviced apartments, hotels or holiday rentals can typically show strong positive cash flow “on paper”. But beware! Often these property types don’t have strong growth fundamentals.

- What’s The Growth Outlook? $20 or even $100 per week in your pocket is nice, but only if growth is also factored into the equation. We scour hundreds of suburbs and thousands of properties to identify properties with strong growth fundamentals.

- Watch Out For Bells And Whistles: by “bells and whistles”, I mean sweeteners such as limited time rental guarantees that make a property cash flow positive, but only as long as the rental guarantee applies. You need to look at what the general rental market will pay after the guarantee expires. And also question why a rental guarantee is being offered in the first place.

- How Is The Positive Cashflow Derived? Remember that positive cash flow properties give you both cash and non-cash tax deductions. Non-cash deductions are depreciation on buildings and fixtures and fittings. However, if the positive cash flow is derived mainly from a huge depreciation schedule, you should be wary.

- Is The Depreciation Claimable? Depreciation of fixtures and fittings is only claimable if you’re the first owner of the property. So if you buy a new property, you can claim these amounts. If you are the second or subsequent owner, you can’t claim these deductions.

- What About Interest Rates? Bank interest is usually a major expense item for property investors, and if interest rates rise substantially, that may turn your positive cashflow property into a neutrally or negatively geared property. So it is prudent to allow for interest rate increases in your modeling, as well as consider fixing your interest rate for a period of time.

- Double Check Your Assumptions: financial models are only as good as the inputs and assumptions that drive them. So if you are expecting a certain rent, conduct due diligence to ensure that rent can be achieved. If you’re expecting growth, make sure the relevant growth drivers are evident in the suburb.

Being aware of potential risks is a natural part of any investor’s due diligence.

Don’t let the risks put you off taking action (because the cost of inaction is huge). However, make absolutely sure you do your homework in order to make high quality decisions.

On that note, let’s talk about…

7. Where To Find Positive Cashflow Properties?

Positive cash flow properties are not always easy to find. Traditionally, cash flow positive properties have had one or more of the following characteristics:

Positive cash flow properties are not always easy to find. Traditionally, cash flow positive properties have had one or more of the following characteristics:

- Located away from capital cities (in regional or rural areas)

- High rental yield (good loan serviceability)

- Lower capital growth (price goes up more slowly)

- Lower purchase price (cheaper to buy)

- In higher risk categories (e.g. mining towns, holiday units etc.)

However, the Australian property landscape has shifted in a way that benefits investors who know where to look.

Several developments – including greater access to property data and lower interest rates – now make it possible to find positive cash flow properties…

- In capital cities or major population centres

- With strong growth potential based on higher demand compared with supply

- With greater security due to the economic diversity of major population centres

In other words, high quality positive cash flow properties are now available in areas that are also poised for growth.

Now let’s look at some of the key criteria to help you locate these high cashflow, high growth gems:

8. Positive Cash Flow Property Due Diligence Checklist

Never before have we had access to as much up-to-date property data. The problem isn’t getting the data. It’s interpreting the data. And then taking action on what that interpretation means.

Never before have we had access to as much up-to-date property data. The problem isn’t getting the data. It’s interpreting the data. And then taking action on what that interpretation means.

Most people look at historical data – things like median price growth over past year.

While these things are helpful, they generally tell you what has already happened in an area.

When looking for pockets of cash flow positive potential, we do take these things into account.

But even more importantly, we look at trends that will affect future prices including:

- Economic Growth: Strong economic growth creates jobs. This attracts people to an area, increasing the demand for housing. And according to the dependable principle of supply and demand, property rents and prices go up.

- Limited Supply: Prices increase the most when demand is strong and supply is limited. That’s why house prices closer to population centres (where land is scarce) tend to rise more than prices in small centres or rural towns (where land is abundant).

- Surrounding Suburbs: A suburb with more expensive neighbouring suburbs often enjoys higher growth. This is known as the “Ripple Effect”. We often look for locations that will benefit from the higher prices in surrounding suburbs.

- Vacancy Rates: Low vacancy rates lead to greater rental demand which means higher prices and less time without a tenant. Vacancy rates of less than 3% are one good indicator of solid rental demand, ensuring your property will never be vacant for much more than 1 or 2 weeks every year.

- Rental Yields: High rental yields boost cash flow. A rental return of around 5% or more is a positive signal.

- Infrastructure: Local amenities have a powerful influence on vacancy rates and rental prices. That’s why we look for locations near schools, universities, shops, transport and other desirable infrastructure. Or even better, locations where infrastructure is being built, but hasn’t yet been priced into local property market values.

- Recent Price Movements: If a suburb has recently doubled in price, it’s unlikely it will double again anytime soon. We study trends and look for suburbs that are set for future growth.

- Valuation: While the true value of a property (or anything for that matter) is the price someone is willing to pay for it, we prefer to take a conservative approach and rely on professional, independent valuations as a reliable guide.

- Potential Tax Benefits: Price is only one factor in a positive cash flow property investment. It’s important to consider all aspects of the equation including the individual property, structure and funding. Depreciation can play an important role in the cash flow equation. That’s why we have a team of experts assessing each positive cash flow property opportunity from all angles.

If you can satisfy the above criteria, then it’s very likely you’re looking at a property that will perform very well in your portfolio over the medium and long term.

And you’re intrigued by the potential of cash flow positive investment property, then you may be wondering what you can do next…

9. How To Take The Next Steps

The tips and advice in this article will help you understand how positive cashflow property works, as well as some of the benefits and risks to consider.

The tips and advice in this article will help you understand how positive cashflow property works, as well as some of the benefits and risks to consider.

One potential option is for you to go it alone and conduct your own research to locate, evaluate, negotiate and purchase the right positive cash flow property for you.

Alternatively, you may want a little help.

If that’s you, then we invite you to request a free, no obligation Property Investment Strategy Session.

During this session, we’ll first seek to understand your situation and goals. Then based on what we discover, we will source well-researched property that is a match for your budget and desired outcomes.

The properties we recommend are typically cash flow positive and located in growth areas close to major population centres.

They are often off-market or exclusive opportunities in small, boutique developments. (We don’t usually recommend apartments, due to their chronic oversupply and poor growth outlook.)

As you know, the property market waits for nobody. It’s no use regretting opportunities that have passed. We hear almost every day from investors who say, “If only I had bought in Location X or Location Y 10 years ago!”.

Now that opportunity has passed and can never be retrieved. However… new opportunities now exist that, 10 years from now, will look like a bargain.

So please make a time to chat to find out what your options are and how Smart Property can help you can grow a profitable property portfolio through positive cash flow properties.