Many property investment books and magazines promote the dream of accumulating a multiple property portfolio. A common strategy goes something like this:

- Acquire your first investment property

- As you build up more equity, refinance and put down a deposit on your next property

- Follow this plan to acquire 10 properties over a long timeframe – perhaps 20 years

- Sell down some of the properties when you retire so you own 5 properties outright, which will provide you with a handsome passive income, indexed to inflation, for the rest of your life

Pursuing a goal like this is admirable – but how many investors actually succeed with this strategy? Not that many, if ATO statistics are anything to go by.

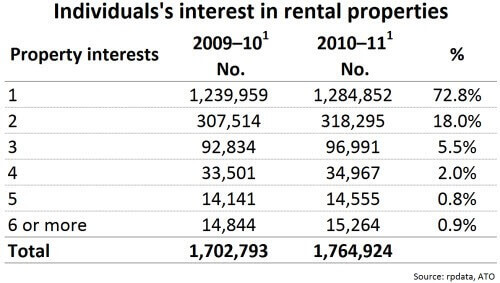

According to this research by CoreLogic, based on RP Data and ATO statistics in the 2010/11 year:

- 14.3% of people who lodged a tax return reported an interest in at least one investment property

- Of the above who are property investors, 72.8% have an interest in just one property

- A further 18% have an interest in two properties

- 9.2% have an interest in three or more properties…

- …and just 0.9% of investors with an interest in six or more properties

I’m not suggesting that investors can’t build a substantial property portfolio or that this isn’t a worthwhile goal. Far from it.

All this shows is that in reality, most investors get derailed along the way. 73% of investors to be exact.

And while you will be vastly better off in retirement if you own one investment property compared to owning zero investment properties, why stop at one if you have the potential to acquire more?

One investment property is great, but as life expectancy increases and the ability for the government to support more and more pensioners diminishes, it’s unlikely that one investment property will be enough. You’ll probably need more to live worry-free in retirement.

So to get to the bottom of how to ensure you don’t get stuck on your first investment property,, we first need to explore…

Why Don’t More Investors Get Past Property #1?

There are many reasons why investors don’t get past their first investment property. Here are a few of the main ones:

Reason #1: They get started too late

Too many investors think about investing for years – sometimes decades – before they actually make it happen. (Even more never make it happen).

Too many investors think about investing for years – sometimes decades – before they actually make it happen. (Even more never make it happen).

Or, they get caught up in paying off their own home instead of investing. While this might sound like a sensible idea, the reality is that this is almost always a terrible strategy for wealth creation.

While due diligence is important and there’s no need to rush out and buy the first property you see, too many would-be investors sit on the fence for years and let opportunity after opportunity pass them by.

And as they wait, their buying power decreases, they miss out on potential equity gains, and their whole property accumulation strategy is destroyed.

The solution is to decide to invest, seek the appropriate knowledge and/or advisors – and then do it.

And if you haven’t started yet, don’t beat yourself up. Like the Chinese proverb says, “The best time to plant a tree was 20 years ago. The second best time is now.”

Reason #2: They never have a PLAN to acquire multiple properties

Michelangelo said, “The greater danger for most of us isn’t that our aim is too high and miss it, but that it is too low and we reach it.”

Michelangelo said, “The greater danger for most of us isn’t that our aim is too high and miss it, but that it is too low and we reach it.”

If you don’t plan to accumulate a property portfolio, you can be almost certain a portfolio won’t suddenly materialise in front of you.

However, an investor who sets a goal to achieve a clear outcome within a predefined timeframe will naturally start to think and act differently.

For example, suppose you set yourself the goal of acquiring 10 properties in 20 years (which is actually very doable, even for investors on average incomes).

The moment you commit to a goal like this, you start to see and do things differently. For example:

- Upgrading your knowledge of property investment, financing and associated strategies by reading books, online learning, workshops etc.

- Ensuring your financial and tax affairs are structured appropriately in order to legally maximise property tax benefits and accelerate the achievement of your desired outcomes

- Following the national property market to decide where your next investment will be

- Regularly reviewing your equity and overall financial situation with a view to making your next purchase

- Implementing strategies to increase the cash flow of your existing property(s)

- Investing in your career or your business in order to increase your value and your earning power

- Keeping your household budget in check and ensuring a chunk of your income goes toward saving and investing

Conversely, many people who don’t set goals (and act accordingly) are constantly scratching their heads wondering where their income goes and why they have very little to show for it.

They’re also the type of people that blame the government, society, or the “big end of town” for making their lives so tough and preventing them from getting ahead.

Reason #3: They lack appropriate education on portfolio building

Building a property portfolio is more complex than acquiring a single property (and yet it’s not rocket science).

Building a property portfolio is more complex than acquiring a single property (and yet it’s not rocket science).

Usually your strategy will involve a variation of the following:

- Acquire one (or more) well-priced properties with good growth prospects and/or good cash flow

- Use market growth, cash flow, rent increases, renovation, surplus income – or a combination of all of the above – to build enough equity to afford a deposit on your next property

- Buy your next property

- Rinse and repeat

Reason #4: Their first property is a dud

Many investors get started on the wrong foot by buying the wrong property. For example:

Many investors get started on the wrong foot by buying the wrong property. For example:

- The property fails to appreciate in value, which makes it hard to “sling shot” you into your next property

- The property generates slugish yield (or even negative yield), reducing your ability to service your next property loan

- The property is hard to rent out, leaving you with reduced income and/or vacancy periods

- The whole experience is sub-par, causing you to be wary of future property investment

The moral of the story is – make sure you buy a good first property! The future of your portfolio depends on it.

We recommend your first property has some or all of these qualities:

- Buy in an area where demand outstrips supply – the law of supply and demand stipulates that when this is the case, property values will go up.

- Buying in your backyard is usually not the answer. Although it’ familiar, the chances of your backyard being one of the highest performing suburbs in Australia are very slim.

- Beware of exotic property types like serviced apartments, holiday rentals or similar – they are at best speculative and often disappoint.

- Be wary of apartments. Apartments easily become over-supplied and may have high body corporate costs that drain your cash flow.

- Buy something relatively “boring” because that’s what performs. By relatively boring, we mean well-located property close to major population centres with growing infrastructure and high owner-occupier demand.

- Cash flow is king. Generally, positive cash flow property with strong growth potential gives you the best of both worlds – a property likely to increase in value that also puts money in your pocket every week. Properties like these accelerate the purchase of your next property.

(By the way, we’re currently working with investors to source very attractive cash flow positive properties that meet the above criteria. Get in touch if you’d like to discuss what may be appropriate for your needs.)

Reason #5: They run out of serviceability

You could purchase even a very good property that is negatively geared and have to wait a long time before you can purchase your next property.

You could purchase even a very good property that is negatively geared and have to wait a long time before you can purchase your next property.

Negative gearing means the property costs you money to hold.

Let’s say a property costs you $15,000 per year to hold after tax benefits. That means, in the banks’ eyes, your income has just been reduced by $15,000.

That may well mean that you are unable to fund the purchase of your next property quickly. So instead of rapidly buying your next property and potentially owning an asset that can increase in capital value while providing cash flow, you’re forced to sit on the sidelines and wait until:

- Your income rises, or

- Rents increase on your first property to reduce your income shortfall, or

- Your first property increases substantially in value, allowing you to revalue, refinance and pull equity out as a deposit on your next property

It’s possible, if you buy very well AND at exactly the right time, that capital growth will allow you to move onto property #2 (and beyond) quickly.

But more often than not, we’ve seen people stagnate on property #1 for longer than they have to.

Having a plan to maintain your serviceability is key to growing your portfolio while mitigating the risks associated with negative gearing.

For this reason, we recommend investors consider positive cash flow property in up and coming growth regions where the “double whammy” effect of both cash flow and growth can sling shot you into your next property.

Following these steps alone will put you among the upper echelons of property investors in Australia, by owning 2+ properties.

To explore our current recommendations for positive cash flow properties, please contact us for an exploratory chat.