Many property owners and potential investors wonder, “Should we pay off our home first, or buy an investment property?”

Sometimes this question is framed in the reverse: “We want to invest in future, but for now we’ll just focus on knocking down the mortgage.”

This question arises frequently enough that we wanted to create a model to compare the two scenarios to see which one leaves you better off (and why).

Here goes:

Scenario 1: Pay Off Your Home First And Invest Later

Take a couple who own their own home, with 20 years remaining on the mortgage:

- Home value: $800,000

- Mortgage balance: $500,000

- Term: 20 years, Principal and Interest

- Interest Rate: 4%

- Repayments: $3,030 per month

- Annual Capital Growth: 7%

Scenario 1 Outcomes:

The loan is paid out in 20 years, by which time the home is worth $3,096,000. Not bad!

Now let’s compare the alternative scenario:

Scenario 2: Start Investing Now, While You Pay Off Your Home

In scenario 2, our couple decide to continue paying down their owner occupied dwelling, while also investing in a cash flow positive property.

Once again, we have the same stats for their home:

- Home value: $800,000

- Mortgage balance: $500,000

- Term: 20 years, Principal and Interest

- Interest Rate: 4% p.a.

- Repayments: $3,030 per month

- Expected Capital Growth: 7%

Then we also add in the following numbers for their cash flow positive investment property:

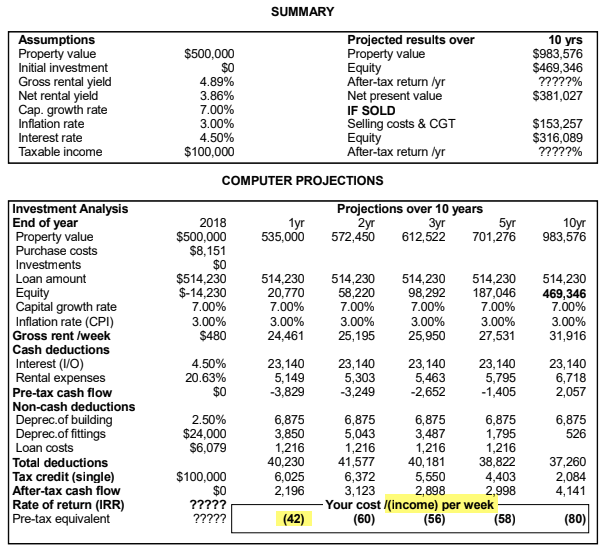

- Investment property value: $500,000

- Mortgage balance (including stamp duty and purchase costs): $530,000

- Term: 30 years, Interest Only

- Interest Rate: 4.5% p.a.

- Cash Flow: $183 per month (or $42 per week in Year 1)

- Expected Capital Growth: 7%

Here’s how the model stacks up:

Notes and Assumptions:

- The owners apply the positive cash flow from their investment property to their owner occupied mortgage.

- The investment property is projected to deliver $42 per week or $183 per month in positive cash flow in Year 1, increasing in subsequent years. However, to be conservative we have assumed the positive cash flow remains at Year 1 levels.

- The owners don’t make any extra repayments from their household budget.

- We assume a 2% annual vacancy rate for the investment property.

- The interest rate for the investment property is higher because the loan type is Interest Only (generally more tax effective for investors).

- In this case, the investors have incomes of $100,000 and $20,000 (relevant for tax purposes).

- The price and cash flow figures are based on actual properties available on today’s market.

Scenario 2 Outcomes:

- By Year 9, equity in the Investment Property would be $405,000

- By Year 9, the remaining balance on the Owner Occupied mortgage would be $299,389

- If the owners decided to sell the investment property in Year 9, the money left after selling costs (including Capital Gains Tax) would be sufficient to pay off the Owner Occupied mortgage in full.

NET OUTCOME:

By using the additional cash flow from their property investment, the owners can pay off their owner occupied mortgage in 9 years instead of 20 years.

After paying off their home, the owners also have an extra $3,030 per month in their pocket every month, for an extra 11 years.

This extra cash could be put toward further investment, or split between a better lifestyle and investment purposes.

The Verdict:

Under most scenarios, investing in property at the same time as paying off your home mortgage is usually a far superior wealth creation strategy than paying off your home mortgage first.

There are three main reasons for this:

- Investing in property now allows you to start accumulating capital gain in that property.

- Property investment is more tax-effective than home ownership in terms of annual tax paid.

- The investment property generates extra after tax cash flow that can be used to knock down the owner occupied mortgage faster.

Some investors perceive paying off their home first to be the “safe” strategy, but in reality this strategy will almost always lead to less financial security, not more.

Of course, it’s also important what type of investment property you purchase. You must buy well to ensure the cash flow and capital gain potential of the investment property delivers the outcome you want.

If you’d like some help creating a property investment plan that fits your situation and goals, please get in touch to arrange an obligation-free Investment Property Strategy Session.